Can shoreline restoration rein in rising flood insurance prices?

by Sydney Cromwell

Some have called Dauphin Island the “Unluckiest Island in America” because it has repeatedly been hit by major hurricanes and storms. But it’s also a place where the residents have tremendous resilience and community strength, Terry Sheffield said, to rebuild after those storms.

“It’s amazing how well this community gets together and rebounds and repairs, and everybody helps everybody out,” said Sheffield, who is the town building inspector and has lived on the island since 2018.

Rebuilding comes with big expenses, however, and most homeowners on Dauphin Island can’t do it without home and flood insurance.

“Where it rains it floods, and the research has shown repeatedly that people who have insurance come back faster,” said Renee Collini, the director of the Water Institute’s Community Resilience Center.

As climate change accelerates sea level rise and increases the intensity of tropical storms, insurance companies are beginning to re-evaluate whether they can afford to insure buildings that are expected to be damaged over and over again.

In some cases, this leads to skyrocketing insurance premiums, which Sheffield said many Dauphin Island residents have experienced. In other cases, insurance companies are leaving vulnerable markets entirely, including other communities on the Gulf of Mexico.

Restoring natural shorelines and coastal ecosystems is considered one of the best ways to lessen the damage from hurricanes and storm surges. Collini is now trying to figure out whether the benefits of those natural shorelines can be translated into insurance savings for Dauphin Island’s homes.

GRAVELINE BAY: A CASE STUDY

Graveline Bay is located on the eastern end of Dauphin Island, which is wider and therefore somewhat less vulnerable to flooding than the narrow spit of the west end. Still, the loss of coastal marsh habitats has made homes near the bay more susceptible to storm damage.

The Town of Dauphin Island contracted the firm Moffatt & Nichol, which has done a number of shoreline restoration projects, to rebuild the coastal marshes that once bordered Graveline Bay.

Like many projects funded by the settlement from the Deepwater Horizon oil spill (through the National Fish and Wildlife Foundation Gulf Environmental Benefit Fund), the Graveline Bay project included extensive measuring and modeling of tides and water levels in the bay both before and after the marsh restoration.

In that data, Collini saw an opportunity to quantify exactly how the newly rebuilt marsh impacted flooding of nearby homes.

Collini’s past work has focused on what prevents people and communities from becoming more resilient to floods and other natural disasters. She knew hard data could potentially convince private insurers and the federal National Flood Insurance Program (NFIP) that the homes near the new marsh now had a lower risk level, which could translate to lower premiums.

“We want to make sure we get credit for the flood risk benefits,” Collini said, even if the primary goal of the project was habitat restoration.

“[Marshes] are so important to our overall quality of life. They play an incredibly important storm mitigation function, but they also play an incredibly important biodiversity function to everything that makes coastal living wonderful.”

Roberta Swann, Mobile Bay National Estuary Program

Since the marsh is small, Collini said the potential premium discount would be modest, akin to renovation projects that make a home more storm-resilient. Still, “as much as everything’s going up in price, every little bit helps,” she said.

And if this model works, she said, it can be applied to other shoreline restoration projects and amplify the impact on insurance affordability.

“This is considered to be a pilot project. This is the first time, or one of the first times, that someone has tried to calculate these benefits and translate them into insurance savings,” said Christina Mohrman, the director of strategic planning and partnerships for the Gulf of America Alliance, which provided funding for Collini’s work.

Moffatt & Nichol finished the Graveline Bay project in September 2023, though monitoring of the site is still ongoing with the help of the Dauphin Island Sea Lab and Alabama Audubon.

Collini is now in the midst of providing data to around 40 nearby homeowners and explaining how to share it with their insurers. She’s hoping within a few months to see whether the insurance discounts become a reality.

WHAT’S EATING DAUPHIN ISLAND

Dauphin Island is in a constant state of change. Mapping over decades has shown the island is narrowing and drifting westward due to the constant pressure of tidal erosion and sand movement.

The east end has lost 100 feet of shoreline in the last three decades, according to a report by the Yale School of the Environment. Since 1975, the narrow west end has eroded at a rate of 3 feet or more per year, according to the Dauphin Island Watershed Management Plan.

Some properties have been completely and permanently submerged.

That’s typical for a barrier island, especially one as narrow as Dauphin Island. But when there are homes and businesses located there, you can’t simply leave the island to the natural course of wind and tides.

Dauphin Island has been directly hit by four major hurricanes in the last century, the most recent being Sally and Zeta in 2020. Other hurricanes that didn’t make landfall there still caused significant damage, as with Katrina in 2005. According to the island’s watershed management plan, more than 80 tropical and subtropical cyclones have affected the Alabama coast since 1951.

Hurricanes Sally and Zeta caused an estimated $3.4 million in damages on Dauphin Island.

“We’re a barrier island. We take the brunt of anything that’s bad and hopefully we slow it down for everyone else,” Sheffield said.

Even seasonal tides and regular storms on the island can create surges or overload stormwater drainage, leading to flooded and damaged buildings, roads covered with sand and debris and more shoreline erosion. These smaller “nuisance floods” can slowly add up to significant damage costs.

“Our spring tides, they’re kind of like storm surges,” Sheffield said.

The Federal Emergency Management Agency (FEMA) considers Dauphin Island to have a “relatively high” risk of floods leading to property loss, according to its Flood Index.

The island is also feeling the effects of rising seas. According to NOAA, the sea level on Dauphin Island has risen about 1.35 feet in the past 100 years. It’s predicted to rise at least another foot by 2050, according to the 2023 National Climate Assessment.

Rising seas mean that each storm surge has the potential to reach higher peaks and travel further inland than it once did, and flood waters will also be slower to recede. Climate Central’s Coastal Risk Finder predicts a 2-foot annual flood on the island by 2030 and a 2.5-foot annual flood by 2050. A 100-year flood would bring 8 feet of water onto the island in 2050, based on current models.

The development of Dauphin Island has also destroyed some of its best defenses. While the town now has stricter building codes to protect marshes, dunes and other sensitive habitats, historical development often occurred on top of those ecosystems by owners seeking waterfront living.

“Everybody wants to have waterfront property, and that waterfront property comes at the expense of these marshes,” said Roberta Swann, the director of the Mobile Bay National Estuary Program.

Graveline Bay, for instance, has lost 75 acres of marshland over the last century or so, according to Moffatt & Nichol.

Wetlands are some of the fastest-disappearing habitats in the world. Trapped between homes and a rising tide, the remnants of Dauphin Island’s marshes are gradually slipping beneath the waves.

“As sea levels rise, there’s nowhere for those marshes to migrate to,” Swann said. “… Our marshes are drowning.”

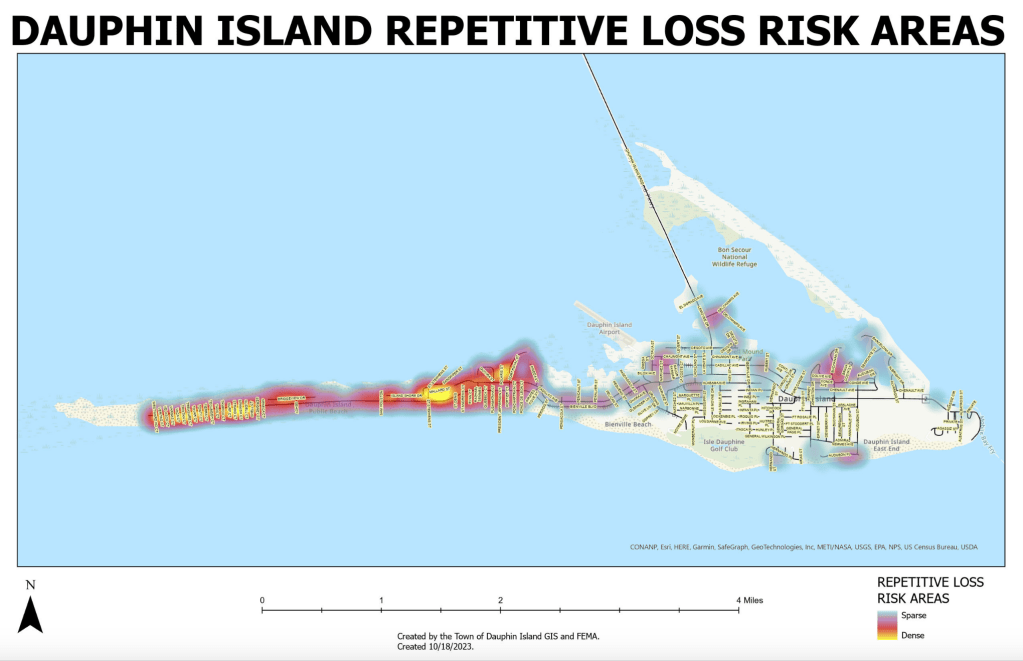

REPETITIVE LOSSES

Homeowners on Dauphin Island and other communities in flood zones need insurance for flood damage in addition to their regular home insurance, since most home policies cover wind damage but not flooding. Those residents can choose a private flood policy or go through the National Flood Insurance Program, which provides coverage even in markets that private insurers consider too risky.

NFIP policies and premiums are determined by the age of a home, the flood zone it’s located in and its elevation. Flood insurance is optional in the low-risk flood zone, but it’s required in the high-risk zones if the owner wants a mortgage or loan for their property.

After severe storms or chronic floods, owners of damaged homes can submit a claim to the NFIP for the cost of needed repairs, just like typical home insurance.

Around 1,700 Dauphin Island properties are insured through the NFIP, according to the island’s watershed management plan. The NFIP insures 4.6 million homes across the country.

Communities that participate in the NFIP are required to enforce certain flood management rules, like requiring permits for development in some flood zones or using specific flood-resistant building materials. Dauphin Island created its flood damage prevention ordinance during the town’s incorporation in 1989.

According to FEMA, Dauphin Island homes built before the NFIP standards have post-storm insurance claims that average around four times higher than homes built since the town adopted the NFIP rules.

“There is a real concern about insurance being available at all. … Affording insurance is one thing, being able to buy it all is another.”

Renee Collini, The Water Institute

The NFIP also has a Community Rating System program, which discounts insurance for buildings that meet higher criteria than the NFIP minimum standards for storm and flood protection, such as elevating a home or putting on a wind-resistant roof.

Sheffield said the town has participated in the CRS program for many years because of its potential insurance savings. The discounts can vary between 5 and 45 percent, depending on the community’s Class Rating and the standards an individual home meets, according to FEMA.

“Any time we can get a participating house built out of harm’s way — storm surges in particular — we’re just going to save loss of life and loss of property,” Sheffield said.

He said most of the buildings on Dauphin Island are meeting at least some of the higher CRS standards.

Since 2018, new homes on the island are required to have roofs that meet the Gold Fortified Standard, meaning they can withstand 200-mile-per-hour hurricane winds.

The Alabama Department of Insurance provides some grant funding for homeowners to replace their roofs to meet the Fortified Roof or Silver Standards, which are lower than the Gold Standard, and the state mandates wind insurance discounts for homes that meet those discounts.

The state has awarded more than $86 million in grants for roof fortification and retrofitting so far. Collini called that funding program a “phenomenal system.”

During 2020’s Hurricane Sally, Collini said wind damage was less than expected in Alabama because of efforts to meet the higher standards. Sheffield said the elevated homes with Gold Standard roofs on the island didn’t receive damage during that storm, though older homes and town infrastructure still took a significant hit.

“There was less damage in Alabama because the overall pool was less risky,” Collini said.

A study released by the state’s Department of Insurance in May found that homes with roofs that met one of the Fortified standards were 55% to 74% less likely to file an insurance claim after Hurricane Sally. The severity of their losses was also lessened.

The study estimated that if every Alabama home impacted by Sally had a Fortified roof, insurers could have saved around $100 million in claim payouts.

Many homes on Dauphin Island are considered “repetitive loss” properties, meaning that they have had two separate flood insurance claims within a decade. A “severe repetitive loss” property has made four or more claims totaling more than $20,000, with at least two happening within a decade of each other.

There are more than 800 repetitive loss structures on Dauphin Island, plus nearly 70 that are considered severe repetitive loss, according to the watershed management plan.

The Yale School for the Environment reports that half of the island’s NFIP insurance claims have been made by only about 100 homes, with a few homes making claims more than 10 times. Dauphin Island has received more than $100 million in FEMA insurance payouts due to storm and flood damage, though exact records aren’t available.

Between 1988 and 2012, Dauphin Island property owners received nearly eight times as much money from the NFIP as they had paid in premiums.

Despite the expense of insuring and rebuilding these properties, the allure of waterfront living keeps drawing new people to Dauphin Island and other coastal American communities.

For the NFIP and private flood insurers, this has become an expensive problem.

AFFORDABILITY CRISIS

Severe weather, from hurricanes to floods to wildfires, is getting more frequent and more intense across the county. The NFIP paid out almost $1 billion in claims in 2023. In Alabama, total insured losses (across all types of property insurance) have doubled from 2013 to 2024.

It’s a situation that the NFIP and private insurance companies weren’t really designed to handle. As the burden continues to mount, everybody — the NFIP, insurers, local governments, homeowners — loses.

Due to the cost of increasing insurance claims during natural disasters and repetitive losses, the NFIP is now $25 billion in debt, after having a previous $16 billion debt cancelled less than a decade ago. According to a report by the New York Times, private insurance agencies in 18 states lost money on property coverage in 2023.

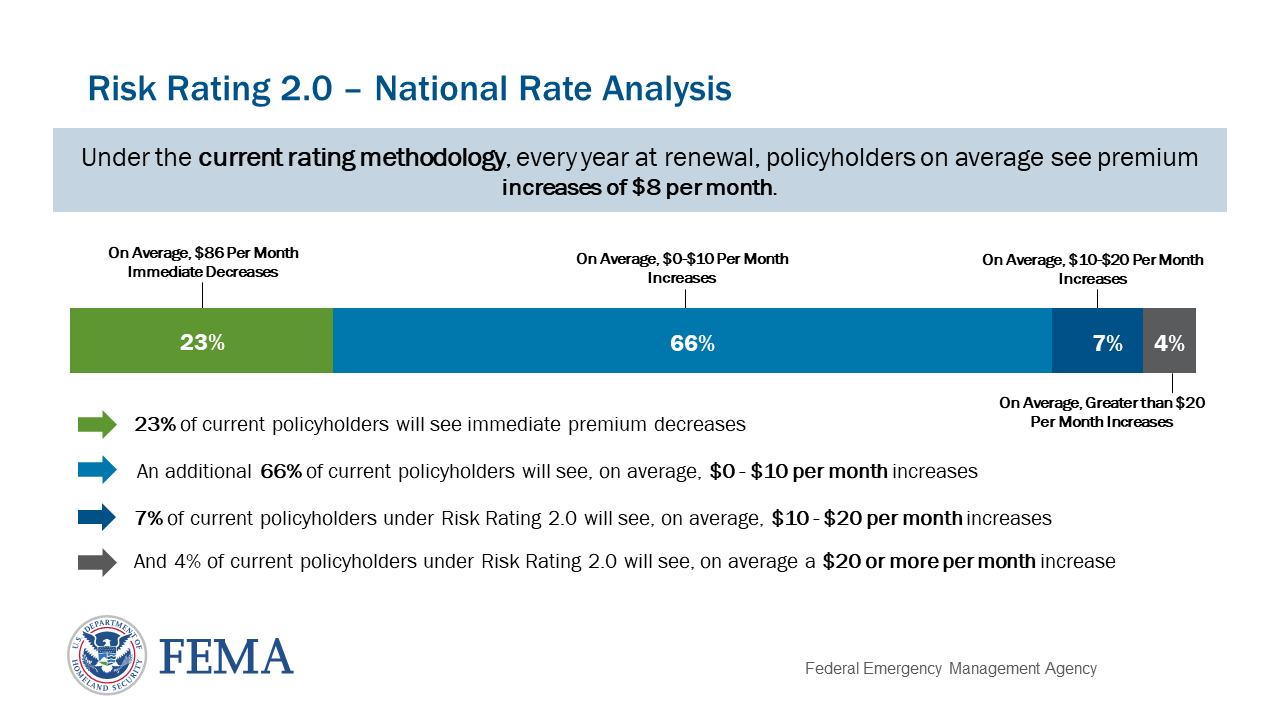

The NFIP responded to this imbalance by introducing the Risk Rating 2.0 system between 2021 and 2023, which updated the program’s methods for determining a property’s actual flood risk and rebuilding costs. According to FEMA, the previous methods were unfairly distributing the cost of rebuilding the most risk-prone homes, and most policies will see their premiums decrease or stay nearly the same.

However, the new rating system means other homes are now considered higher risk and their premiums are going up. FEMA estimated that almost 82% of homes in Dauphin Island’s zip code (36528) would see premium increases within the first year, though the vast majority would increase by less than $10 per month.

“Flood insurance rates are already high, but they’re expected to increase even more,” Mohrman said.

Dauphin Island’s watershed management plan predicts annual NFIP premium increases due to the new rating system could continue for about two decades.

Private insurers are also raising premiums based on their own risk determinations. Companies have chosen to leave certain markets in California, Florida and Louisiana because they can no longer make a profit covering more and more repetitive losses. Some insurance companies folded after the expensive 2020 and 2021 hurricane seasons.

“There is a real concern about insurance being available at all,” Collini said. “… Affording insurance is one thing, being able to buy it all is another.”

“Where it rains it floods, and the research has shown repeatedly that people who have insurance come back faster.”

Renee Collini, The Water Institute

Sheffield said he regularly hears from residents who can’t afford their insurance premiums. Some choose to forgo home or flood insurance altogether.

“On the island, there’s a wide range of socioeconomic situations, and across all of those we’re seeing insurance become either painfully expensive or impossible to afford, and people are forced to drop it,” Collini said.

NBC News reported last year that around 17.6% of Alabama homeowners — around 250,000 households — lack home insurance.

Based on current models of climate change and sea level rise in the near future, the trend of rising premiums and uninsurable communities will probably continue.

It’s a bleak picture for Dauphin Island’s residents, and something has to be done to make insurance more affordable.

“Basic flood insurance is unobtainable due to the cost. So the little projects we’ve done to protect that from wind and wave action, it should help these individuals get a discount on their flood insurance,” Sheffield said.

HOW MARSHES PROTECT HOMES

The CRS program’s recommendations often focus on improvements that can be made to protect a single building. Restoring a marsh or shoreline, on the other hand, can have community-scale impacts.

Coastal marsh habitats, like the one rebuilt in Graveline Bay, are able to slow down wave energy and reduce the amount of water that travels inland.

“The marshes are able to act like a sponge. They knock that down, they reduce that energy,” Collini said.

By their very nature, these habitats are able to withstand being covered completely by a storm surge and bounce back afterward, Swann said.

“That is the first line of defense,” she said.

When the MBNEP does a marsh restoration, “we’re designing them to be able to be submerged and come back to life,” Swann said.

These living shoreline projects can mean restoration of marshes or sand dunes, like in Graveline Bay, but they can also include stabilizing and protecting the existing habitat from threats, or adding sand and sediment to the shoreline to expand it (called “renourishment”).

Swann said the MBNEP has spent the past several years encouraging local governments to think of coastal marshes as a piece of their town’s infrastructure, like a road: They need maintenance and funding in order to provide their full benefits.

“They’re so important to our overall quality of life. They play an incredibly important storm mitigation function, but they also play an incredibly important biodiversity function to everything that makes coastal living wonderful,” Swann said.

The Town of Dauphin Island has put increased focus on protecting and rebuilding these habitats in recent years. The town approved a new wetland ordinance in August 2022 that outlined steps property owners should take to protect vulnerable habitats, as well as fines for violations.

New construction now has to leave a certain amount of vegetation intact, Sheffield said, and there are more protections for the island’s sand dunes. The town also no longer allows mobile homes, and new construction has to be raised a certain amount above flood level.

“There’s real thought going into how do we keep people safe,” Collini said.

The town has also recently funded projects similar to the Graveline Bay restoration, such as restorations on Little Dauphin Island, two living shorelines in Aloe Bay, refilling sand on the north shore and beach and dune renourishment on both ends of the island.

The Mobile Causeway project includes rebuilding about 80 acres of marshes and rocky breakwater habitats and protecting 300 acres of existing marsh around the highway that connects Dauphin Island to the mainland. The causeway is frequently damaged or submerged by storm events, which cuts off rescue and rebuilding resources from the island in the immediate aftermath.

According to Mobile County’s website for the project, its completion will restore the eastern shoreline of the causeway to its 1917 boundaries

Sheffield said they’re seeing the benefits from these projects already. New “humps” built in certain parts of the west end, for instance, have kept water and sand off the roads, he said, reducing the amount the town has to spend on clean-up efforts. They want to extend those protections across the rest of the west end over time.

There have also been learning curves. Sheffield said in one of the town’s first beach renourishment projects, much of the new sand had washed out to sea within two years due to a hurricane. It’s a common problem with beach renourishment, though Sheffield said more recent attempts to add to the shoreline have lasted longer.

And in some places, particularly on the narrow west end, adding more sand can’t do enough to protect homes.

“There are some areas where that won’t work, and we do have a couple seawalls on the far west end that have basically held the west end,” Sheffield said. “… If it wasn’t for the seawalls, that would probably be cut in two.”

Shoreline projects are expensive, which Swann said has been a repeated obstacle.

“All of this takes money, and we don’t have money on a regular basis to invest in these types of natural systems,” she said. She noted that the Deepwater Horizon settlement funds have helped pay for these projects and demonstrate their value to coastal municipalities.

Dauphin Island spent an estimated $22 million in federal funding on beach nourishment projects in 2024, according to Western Carolina University’s beach nourishment tracker. The west end nourishment project is likely to cost around $60 million by the time it’s completed, according to the project website, and the east end nourishment has $30 million in federal funds. The Mobile Causeway project is also expected to cost more than $30 million.

The Aloe Bay living shorelines have more than $5.2 million in funding. The work done in Graveline Bay cost around $6.4 million.

PROTECTIVE AND PRODUCTIVE

In Graveline Bay, the Moffatt & Nichol team went with a “marsh mound” approach to rebuilding the shoreline.

They constructed a series of mounds over 60 acres, using dredged sand and other sediment from nearby. The 10 largest mounds are located farthest out in the bay, and they’re meant to withstand the greatest amount of wave energy and erosion, dampening the impact on the smaller mounds behind them.

Each mound was planted with native flowers and grasses, which help hold the mounds in place and slow down the movement of water. According to town reports, a total of 87,000 plants were included in the project, plus 600 cubic yards of oyster shell placed underwater in the bay for additional habitat.

There is space between each mound for water to flow at high and low tides, which creates important nursery habitats for many of the aquatic species around Dauphin Island.

“The goal for this project was, how can we maximize the most ecological productivity,” coastal engineer Peyton Caraway said. “… We do want that tidal connection throughout the site.”

When they were designing the project, Caraway said the firm factored in conversations with Graveline Bay residents, as well as tidal and sea level rise data from NASA and NOAA.

Moffatt & Nichol coastal scientist Meg Goecker said some residents wanted the project to include dredging a nearby channel for better boat access, but the channel wasn’t under town control and couldn’t be included. They did modify their design to avoid blocking personal boat channels that people had made, she said.

“The goal of the project was to create habitat that has been lost, and we met those goals and tried to make as many people as we can happy,” Goecker said.

For a federally funded project, the Graveline Bay restoration happened in “record time,” Goecker said. Since the U.S. Army Corps of Engineers and U.S. Geological Survey had previously assessed Dauphin Island’s need for these types of restorations, she said, getting permits and funding took less than half the time it usually does.

Still, completing the entire design, engineering and construction process still took several years of work.

“Marine construction isn’t simple. We’re talking about dredges and pipelines,” Goecker said.

In the spring following the project’s completion, Sheffield said several nearby residents reported less home damage during storms, though the roads did still flood.

“When we had water coming up in people’s houses, people said it didn’t get as bad,” Sheffield said.

Goecker said she also heard from one resident who was pleased that storms were no longer damaging her dock or dragging debris into her yard.

“People’s property is safer, so regardless of what it does for insurance, that’s better,” Collini said.

Since the restoration’s completion, Caraway said they’ve continued monitoring how the dredged material settles over time, how wildlife use the site and whether the native plants survive.

Monitoring will wrap up this fall. The ways that the marsh has changed since it was rebuilt will provide valuable insights for future projects, Goecker said.

“A lot of projects never get to monitor, and so we never get to learn,” she said.

‘SCREAMING IT FROM THE ROOFTOPS’

Collini, meanwhile, is gaining her own insights from the monitoring data.

She’s in the midst of refining down the Graveline Bay data into something simple that shows homeowners the range of potential discounts they could get on their insurance premiums from their reduced flooding risk.

The Community Resilience Center will then help property owners talk with their insurance agents and formally submit data as needed, she said.

Collini said she plans to reach back out a few months later and see if anyone actually achieved a lower premium. Since there haven’t been many similar projects to connect natural risk reduction to insurance premium reduction, she’s still figuring out the best process.

“We are suspicious that they [insurance agents] won’t know what to do with it, or that FEMA won’t do anything with it,” Collini said. “… I don’t know that from a process perspective it’s fully been hammered out.”

There are also still uncertainties to be faced with the new Risk Rating 2.0 program and ongoing changes to FEMA’s authority, which have disrupted her plans. Project 2025 advisors, many of whom are now part of the presidential administration, had even floated the idea of getting rid of the NFIP prior to President Donald Trump’s re-election.

“Some of this may not work out the way we expected,” Collini said.

“This is the first time, or one of the first times, that someone has tried to calculate these benefits and translate them into insurance savings.”

Christina Mohrman, Gulf of America Alliance

If none of the Graveline Bay residents see a change in their insurance costs, Collini said she plans to follow up directly with FEMA to find out the next steps they should take.

“It’s anticipated that not everybody is going to be able to get a reduction because this is a new process,” Mohrman said, though she added that the team will try to troubleshoot and understand the rejections.

“Our goal is that we come up with the process, we understand the process of how to get risk reduction measures … better integrated into the Risk Reduction 2.0 process,” Collini said.

And if they succeed?

“If we figure out that process, we want to share it far and wide, screaming it from the rooftops — let everyone in on the secret,” Collini said.

LONG-TERM LIVABILITY

A rebuilt marsh like the one in Graveline Bay isn’t intended to last forever. Like the rest of the island, the bay is constantly, imperceptibly changing.

“There’s no telling what it will look like in the next 100 years,” Collini said.

With the continual influence of wave erosion and rising seas, Goecker said they design shoreline restorations to last about 20 to 25 years. Swann said the MBNEP’s restoration projects generally have the same lifespan before they become completely submerged.

“We try to design our projects to reach that sweet spot of intertidal [zone] as long as possible,” Caraway said.

The monitoring by the Sea Lab helps them figure out ways to protect the marsh for as long as possible, but they’re always fighting the inevitable.

“We can only tell the future so much,” Goecker said. “… You wouldn’t ever want to promise 50 years.”

That means some shorelines will eventually have to be rebuilt again, and the insurance benefits they bring will have to be reassessed.

Sheffield said Dauphin Island’s building codes also have to change as the island changes. The town is currently in the process of updating most of its codes from 2018 to 2024 standards, he said.

The town has allowed an additional foot of height on seawalls in response to sea level rise, to prevent water spilling over the walls and getting trapped behind them. In the near future, he said, they’ll probably have to reassess the rate of sea level rise and see if codes need to change again in response.

“Eventually, we’ll probably have to raise it,” Sheffield said of the height limit on seawalls. “… We’re aware of it, we’re working on it.”

As coastal living becomes more expensive and more prone to natural disasters, some researchers and experts in the world of insurance and emergency management are turning the discussion to relocation rather than rebuilding. In the long term, they say, vulnerable places like Dauphin Island may simply not be livable.

“I think what’s considered habitable depends on who you ask,” Collini said.

Relocation, sometimes called “managed retreat,” can be controversial both for politicians and for property owners in high-risk zones. Federal funds are more available for rebuilding than for relocating, and property owners on Dauphin Island have been denied in the past. Some research has indicated that buyout funds aren’t reaching the low-income residents who most need the assistance to move somewhere safer.

Despite the risks, waterfront property still holds high value, leading to new construction even as other homeowners consider buyouts.

Plus, there are the emotional ties that residents have to living on Dauphin Island, particularly if it’s been their family’s home for multiple generations, Collini said.

“This is one way that we can help support people continuing to live on the coast,” Mohrman said of the Graveline Bay insurance project. “… It’s important that we have affordable and resilient housing.”

Collini said she doesn’t feel it’s her place to decide for people whether Dauphin Island is livable in the long term, or even how they define “long term.”

“My work is to make sure people are informed, not to tell people what to do or where to go, but to make sure people have all the information they need,” she said.

Main article image of Graveline Bay by Fly the Coast, courtesy of Meg Goecker.

{kind=link}

3 thoughts on “Marsh insurance”